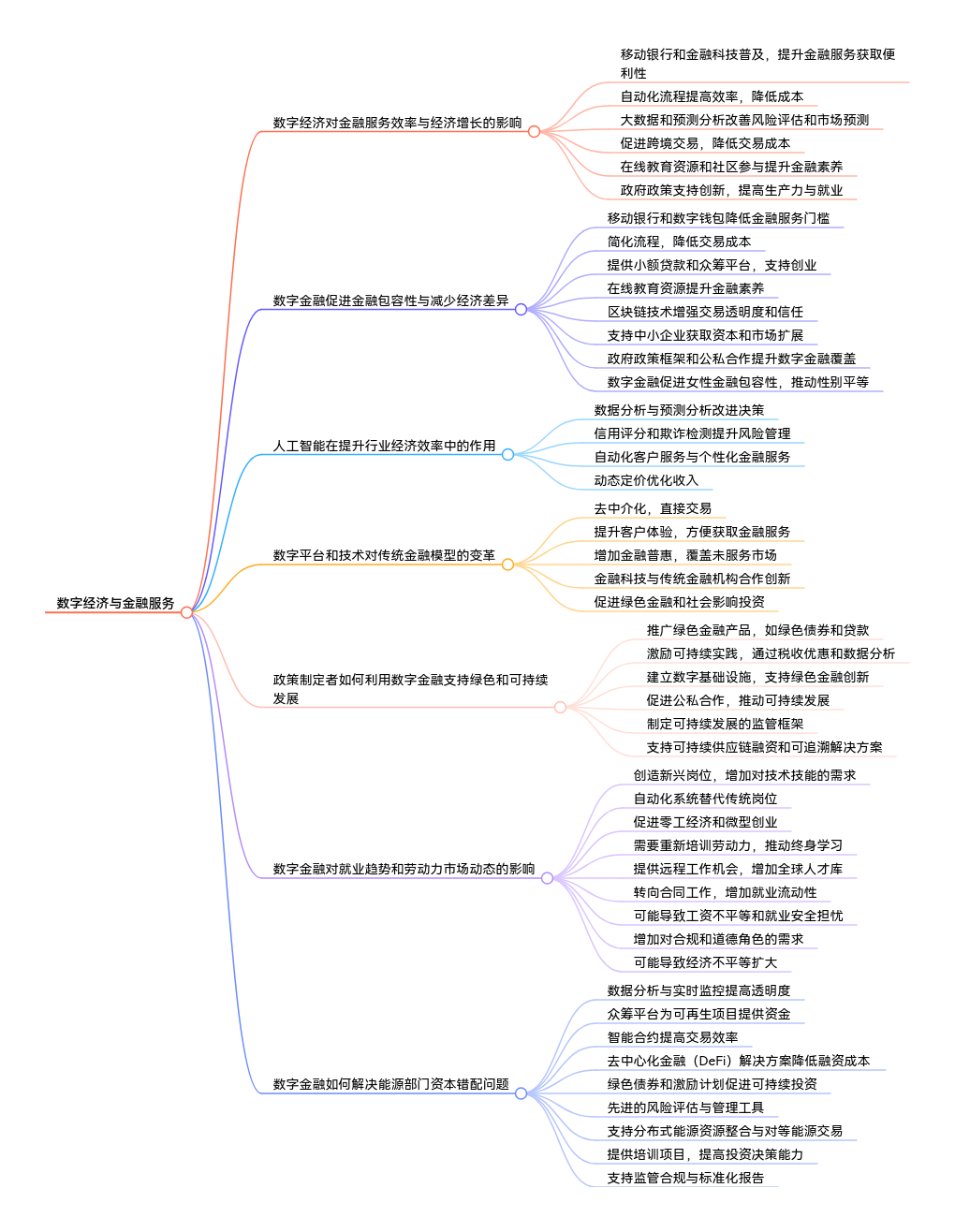

Mobile Banking/fintech: The proliferation of smartphones enables mobile banking, allowing individuals and businesses in remote areas to access financial services easily.

Increased Efficiency and Cost Reduction

Automation of Processes: Digital tools automate various financial processes (e.g loan approvals, transaction processing), reducing operational costs and time.

Improved Data Analytics and Risk Assessment

Big Data Utilization(使用): Financial institutions can leverage big data analytics to assess credit risk more accurately, enabling better lending decisions.

Predictive Analytics: AI-driven analytics help predict market trends and customerbehavior, allowing for proactive financial product offerings.

Facilitation of Cross-Border Transactions(便利跨境交易)¶

Global Connectivity: The digital economy enables easier cross-border transactions, facilitating trade and investment between emerging markets and developed economies.

Lower Transaction Costs: Digital platforms often reduce the costs associated with, international payments, making it easier for businesses to operate globally.

Promotion of Financial Literacy

Online Education Resources: Digital platforms offer resources and tools to improve financial literacy, empowering individuals to make informed financial decisions.

Community Engagement: Social media and online forums facilitate discussions about financial products and services, enhancing understanding and engagement.

Digital Policies: Governments in emerging markets are increasingly adopting digital policies to support the growth of the digital economy, enhancing the regulatory framework for fintech.

Incentives for Innovation: Supportive regulations and incentives for startups encourage innovation in financial services, driving competition and improving service quality.

lmpact on Economic Growth

Increased Productivity: Enhanced financial services contribute to higher productivity levels in various sectors, driving overal economic growth.

Job Creation: The growth of digital financial services creates new job opportunities in tech, finance, and related sectors, contributing to economic development.

Question2: How can digital finance promote financial inclusion(包容性) and reduce economic disparities(差异) indeveloping countries?¶

Reduced Costs: Digital finance often has lower transaction fees compared to traditional banking, making it more affordable for low-income individuals to access financial services.

Simplified Processes: The application processes for loans andother financial products are often streamlined and can be completed online, reducing the time and effort reguired.

Microloans: Digital platforms provide microloans to entrepreneurs and small businesses, enabling them to invest in their ventures and improve their livelihoods.

Crowdfunding: Peer-to-peer lending and crowdfunding platforms allow individuals to raise funds for projects or businesses, democratizing access tocapital.

Online Resources: Digital finance platforms often provide educationala resources and tools to improve financial literacy, empowering individuals to make informed financial decisions.

Community Engagement: Social media and online forums facilitate discussions about financial products, helping to demystify finance for marginalized groups.

Transparency:Technologies like blockchain enhance transparency in transactions, fostering trust among users and encouraging participation in the financial system.

Access to Capital: Digital finance provides SMEs with easier access to credit, enabling them to grow and create jobs, which is essentia for economic development.

Market Expansion: E-commerce platforms allow SMEs to reach abroader customer base, enhancing their sales potential and contributing to economic growth.

Policy Frameworks: Governments can create supportive regulatory environments that encourage the growth of digital finance, ensuring that underserved populations benefit from these services.

Public-Private Partnerships: Collaborations between governments, NGOs, and fintech companies can enhance the reach and impact of digital finance initiatives.

Women's Financial Inclusion: Digital finance solutions can specifically target women, offering them access to financial services that were previously unavailable,thus promoting gender equality.

Empowerment: Access to finance empowers women to start businesses, invest in education, and improve their families' economic status.

Question3: What role does artificial intelligence play in enhancing the economic efficiency of industries through digital finance?¶

Data Analytics: Al algorithms analyze vast amounts of financial data to identify trends, patterns, and insights, enabling businesses to make informed decisions quickly.

Predictive Analytics: Al can forecast market trends and consumer behavior, helping companies anticipate changes and adjust their strategies accordingly.

Credit Scoring: Al enhances credit risk assessment by analyzing non-traditional data sources (like social media activity), leading to more accurate credit scoring and lending decisions.

Fraud Detection: Machine learning models can detect unusual patterns in transactions, identifying potential fraud in real-time and reducing financial losses.

Al-powered chatbots and virtual assistants provide 24/7 customer support, handling inquiries efficiently and freeing up human resources for more complex tasks.

Al analyzes customer data to offer personalized financial products and services, increasing customer satisfaction and loyalty.

Dynamic Pricing

Al can adjust pricing models in real-time based on demand, competition, and customer behavior, optimizing revenue.

Question4: In what ways can digital platforms and technologies transform traditional financial models and business practices?¶

Digital platforms and technologies are revolutionizing traditional financial models and business practices in several impactful ways. Here are some key transformations:¶

Disintermediation

Direct Transactions: Digital platforms enable direct transactions between consumers and service providers, reducing the need for intermediaries like banks and brokers.

Peer-to-Peer (P2P) Services: P2P lending and crowdfunding platforms allow individuals to lend and invest directly, bypassing traditional financial institutions.

Enhanced Customer Experience

User-Friendly interfaces: Digital platforms provide intuitive interfaces, making financial services more accessible and easier to navigate for consumers.

24/7 Access: Customers can access financial services anytime and anywhere, improving convenience and satisfaction.

Increased Financial inclusion

Access to Underserved Markets: Digital technologies enable financiaservices to reach unbanked and underbanked populations, promotingfinancial inclusion.

Microfinance Solutions: Platforms offering microloans and small-scale financial products empower entrepreneurs and small businesses in developing regions.

Collaboration and Ecosystem Development

Fintech Partnerships: Traditional financial institutions are collaborating with fintech companies to innovate and enhance their service offerings.

Open Banking: APls allow third-party developers to create applications that interact with banks, fostering a collaborative ecosystem that enhances customer choices.

Sustainability and Ethical Practices

Green Finance: Digital platforms can promote sustainable investing by providing transparency on environmental, social, and governance(ESG) factors.

Social Impact Investing: Technologies enable investors to support projects with social benefits, aligning financial returns with positive societal outcomes.

Question5: How can policymakers leverage digital finance to support green and sustainable economic development?¶

Policymakers can leverage digital finance to support green and sustainable economic development through various strategies and initiatives. Here are some effective approaches:

Promoting Green Financial Products

Green Bonds and Loans: Encourage the issuance of green bonds and loans through digital platforms to finance environmentally friendly projects, such as renewable energy and sustainable infrastructure.

Sustainable Investment Funds: Foster the creation of digital investment platforms that focus on ESG (Environmental, Social, andGovernance) criteria, making it easier for investors to support sustainable initiatives.

Incentivizing Sustainable Practices

Tax incentives:implement tax breaks or incentives for businesses and individuals who invest in green technologies and sustainable practices, facilitated through digital finance tools.

Data-Driven Policy Making

Big Data Analytics: Utilize data analytics to assess the environmental impact of financial activities and identify opportunities for sustainable investments.

Building Digital Infrastructure

Investment in Digital Tools: Promote the development of digital tools and platforms that facilitate access to green finance such as apps for tracking carbon footprints or platforms for trading carbon credits.

Support for Fintech innovations: Encourage fintech companies to innovate solutions that promote sustainability, such as apps that reward users for eco-friendly behaviors.

Fostering Public-Private Partnerships

Collaboration with Fintech: Partner with fintech companies to develop products that support sustainability, leveraging their expertise in technology and customer engagement.

Engagement with NGOs: Collaborate with non-governmental organizations to promote awareness of green finance options and educate communities about sustainable practices.

Regulatory Frameworks for Sustainability

Establishing Standards

Encouraging Responsible Lending: Implement regulations that require financial institutions to consider environmental impacts in their lending practices.

Capacity Building and Education

Financial Literacy Programs

Training for Financial Institutions

Encouraging Sustainable Supply Chains

Digital Supply Chain Financing: Promote digital finance solutions that support sustainable supply chains, enabling businesses to financeeco-friendly practices through out their operations.

Traceability Solutions: Support technologies that enhance traceability in supply chains, ensuring that products meet sustainability standards.

Question6: What are the implications of digital finance on employment trends and labor market dynamics in the digital economy?¶

Job Creation in Fintech and Digital Services

Emerging Roles: The growth of fintech companies creates new job opportunities in areas like data analysis, cybersecurity, blockchain development, and digital marketing.

Increased Demand for Tech Skills: As financial services become more digitized,there is a rising demand for employees with technical skills,including software development and data science.

Displacement of Traditional jobs

Automation of Routine Tasks: Many traditional roles in finance, such as tellers and customer service representatives, are being replaced by automated systems and Al-driven solutions.

Gig Economy (零工经济) Expansion

Freelancing Opportunities: Digital finance facilitates the gig economy by enabling freelancers to manage payments and contracts through online platforms, increasing flexible work opportunities.

Micro-Entrepreneurship: Individuals can leverage digital finance tools to start small businesses, leading to a rise in self-employment and entrepreneurial ventures.

Skills Gap and Workforce Development

Need for Reskilling-Lifelong learning: Workers in traditional finance roles may need reskilling to transition to new roles in the digital economy, creating a demand for training programs and educational initiatives.

Remote Work Opportunities

Flexibility and Accessibility: Digital finance enables remote work, allowing employees to work from various locations, which can lead to a more diverse workforce.

Global Talent Pool: Companies can hire talent from around the world, increasing competition and potentially driving down wages for certain roles.

Changing Employment Relationships

Shift to Contractual Work: There is a growing trend toward contractual and project-based work rather than permanent employment, altering the traditional employer-employee relationship.

Increased job Fluidity: Workers may move between jobs and projects more frequently, leading to a more dynamic labor market.

Impact on Wages and job Securit

Wage polarization: the demand for high-skilled workers may lead to wage increases for those with the necessary skills, while low-skilled workers may face stagnant wages or job insecurity.

Job Security Concerns: The rise of automation and gig work can lead to concerns about job security and benefits traditionally associated with full-time employment.

Regulatory and Compliance Roles

Increased Regulatory Oversight: As digital finance grows, there will be a need for professionals who specialize in regulatory compliance, risk management, and cybersecurity, creating new job opportunities.

Focus on Ethical Practices: There will be a demand for roles focused on ethical considerations in digital finance, including transparency and consumer protection.

lmpact on Economic inequality

Potential for Increased Ineguality: lf access to digital finance and the skils reguired to thrive in the digital economy are not equitably distributed, economic inequalty may widen.

Quesition7: How can digital finance address the challenges of capital misallocation and improve resource efficiency in the energy sector?¶

Enhanced Data Analytics and Transparency

Real-Time Data Monitoring

Improved Transparency

Crowdfunding for Renewable Projects

Access to Capital: Digital platforms can facilitate crowdfunding for renewable energy projects, allowing individuals and small investors to contribute to initiatives that may otherwise struggle to secure funding.

Diverse Funding Sources: By broadening the investor base, crowdfunding can reduce reliance on traditional financing methods, which may lead to misallocation of capital.

Smart Contracts for Efficiency

Automated Transactions: Smart contracts can automate the execution of agreements based on predefined conditions, reducing administrative costs and inefficiencies in project financing.

Performance-Based Payments: Payments can be linked to actual performance metrics(e.g., energy output),ensuring that funds areallocated based on results rather than estimates.

Decentralized Finance (DeFi) Solutions

Peer-to-Peer Lending: DeFi platforms can enable direct lending for energy projects, reducing the need for intermediaries and lowering costs,which can lead to more efficient capital allocation.

Incentivizing Sustainable Practices

Green Bonds: Digital finance can facilitate the issuance of green bonds that fund environmentally friendly projects, ensuring that capital is directed towards sustainable energy initiatives.

Incentive Programs: Financial incentives for energy efficiency improvements can be tracked and managed through digital platforms, promoting better resource utilization.

Risk Assessment and Management

Advanced Risk Modeling: Digital finance tools can utilize big data and AI to assess risks associated with energy investments, leading to more informed capital alocation decisions.

Insurance Products: Digital finance can facilitate the development of innovative insurance products that cover specific risks in the energy sector, encouraging investment in new technologies.

Integration of Renewable Energy Sources

Distributed Energy Resources (DER): Digital finance can support the integration of DERs, such as solar panels and wind turbines, into the energy grid, improving overall efficiency and resource utilization.

Energy Trading Platforms: Digital platforms can enable peer-to-peer energy trading, allowing consumers to buy and sell excess energy, optimizing resource allocation within local grids

Capacity Building and Education

Training Programs: Digital finance can support educational initiatives that help stakeholders understand financing options for energy projects, leading to better investment decisions.

Awareness Campaigns: Promoting awareness of available digital financial tools can empower investors and proiect developers to make informed choices, reducing capital misallocation.

Regulatory Frameworks and ComplianceSupport for Regulatory Compliance: Digital finance canstreamline compliance processes for energy projects, ensuring thatcapital is allocated to projects that meet regulatory standards

Standardization of Reporting: Establishing standardized reporting metrics for energy projects can improve transparency and accountability, reducing the likelihood of misallocation.

¶

¶ ¶

¶ ¶

¶ ¶

¶ ¶

¶ Government and Regulatory Support¶

Government and Regulatory Support¶ Promoting Gender Equality¶

Promoting Gender Equality¶ ¶

¶ ¶

¶